SOURCE:

PMIs Signal Eurozone Recession Day After First ECB Rate-Hike In 11 Years | ZeroHedge

A day after Christine Lagarde hiked EU rates by 50bps (the first increase in rates in over a decade), S&P Global's Flash Eurozone Composite PMI unexpectedly plunges into contraction.

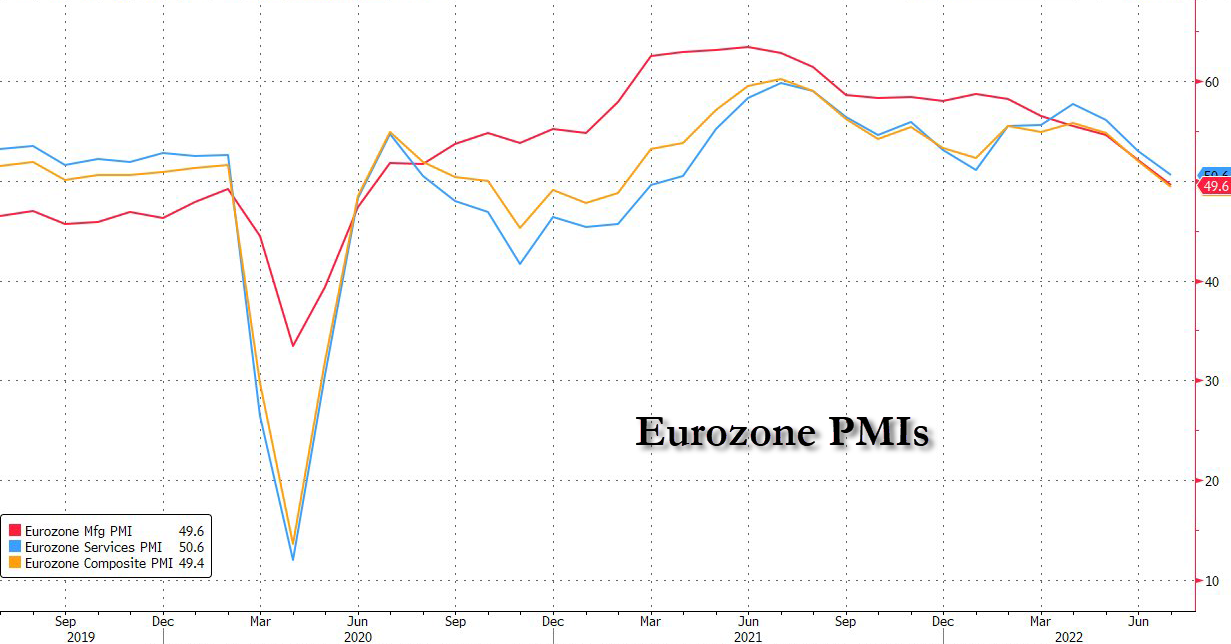

Against expectations of a small weakening (from 52.0 to 51.0), the flash EZ Composite PMI tumbled to 49.4 (below 50 signaling contraction) in July, with manufacturing bearing the brung of the pain for now...

Flash Eurozone Services PMI Activity Index at 50.6 (Jun: 53.0). 15-month low.

Flash Eurozone Manufacturing Output Index at 46.1 (Jun: 49.3). 26-month low.

Flash Eurozone Manufacturing PMI at 49.6 (Jun: 52.1). 25-month low.

Commenting on the flash PMI data, Chris Williamson, Chief Business Economist at S&P Global Market Intelligence said:

“The eurozone economy looks set to contract in the third quarter as business activity slipped into decline in July and forward-looking indicators hint at worse to come in the months ahead.

“Excluding pandemic lockdown months, July’s contraction is the first signalled by the PMI since June 2013, indicative of the economy contracting at a 0.1% quarterly rate. Although only modest at present, a steep loss of new orders, falling backlogs of work and gloomier business expectations all point to the rate of decline gathering further momentum as the summer progresses.

“Of greatest concern is the plight of manufacturing, where producers are reporting that weaker than expected sales have led to an unprecedented rise in unsold stock. Production will likely need to be reduced as companies adapt to this weaker demand environment, in turn widely linked to rising prices.

“In services, the boost to demand from the reopening of the economy has faded and growth is now at a near standstill, with customers often deterred by the increased cost of living and concerns about the outlook.

“Business expectations for the year ahead have meanwhile fallen to a level rarely seen over the past decade as concerns grow about the economic outlook, fuelled in part by rising worries over energy supply and inflation but also reflecting tighter financial conditions.

“With the ECB raising interest rates at a time when the demand environment is one that would normally see policy being loosened, higher borrowing costs will inevitably add to recession risks.

“One ray of light was a further marked cooling of inflationary pressures from the survey gauges of both input costs and selling prices, which should feed through to lower consumer price inflation. However, at present, these inflation gauges remain higher than at any time prior to the pandemic, underscoring the unenviable challenge facing policymakers of taming inflation while avoiding a hard landing for the economy.”

As a result of this, EU bond yields have puked lower with 10Y Bunds now down a stunning 35bps from yesterday's highs...

And 2Y German yields crashed by the most 'since Lehman' in 2008...

How long before Christine flip-flops back to negative rates?

The market is pricing in ECB rate-cuts by May of next year.

No comments:

Post a Comment

Note: Only a member of this blog may post a comment.