SOURCE:

Does the small-cap effect really exist? | TEBI (evidenceinvestor.com)

I have been going on about the existence or non-existence of systematic risks factors like value or momentum for so long, that all my readers will by now be familiar with the seminal paper by Cam Harvey, Yan Liu and Heqing Zhu where they test more than 300 different risk factors identified in the literature. I feel like I link to it about once a month, mostly when it comes to looking in data for systematic effects. If you use the same underlying data for all kinds of tests, chances are that more often than not you will find a statistically significant risk factor by pure coincidence.

The key problem is that most studies on risk factors are done with the CRSP data for US stocks. This data has the tremendous advantage of being extremely comprehensive and extremely “clean”, i.e. the numbers are free from errors and missing data. The problem with the CRSP data is that it covers only the period from 1926 onwards, so we don’t really know if our observations hold before then.

But this is also a huge opportunity. If we can identify factors in the CRSP data and then test these factors with stock market data for the years before 1926, we can create an out of sample test. If the factors also show up before 1926 it gives us a strong indication that these factors are real. If they disappear in the pre-1926 data we may have some doubts about these factors. Surely, there are many reasons why a factor may not have existed before 1926 since equity markets were very different back then but if a factor disappears in the pre-1926 data we should at least start to investigate why it does disappear and not just dismiss the falsification as irrelevant. Remember: Trust, but falsify.

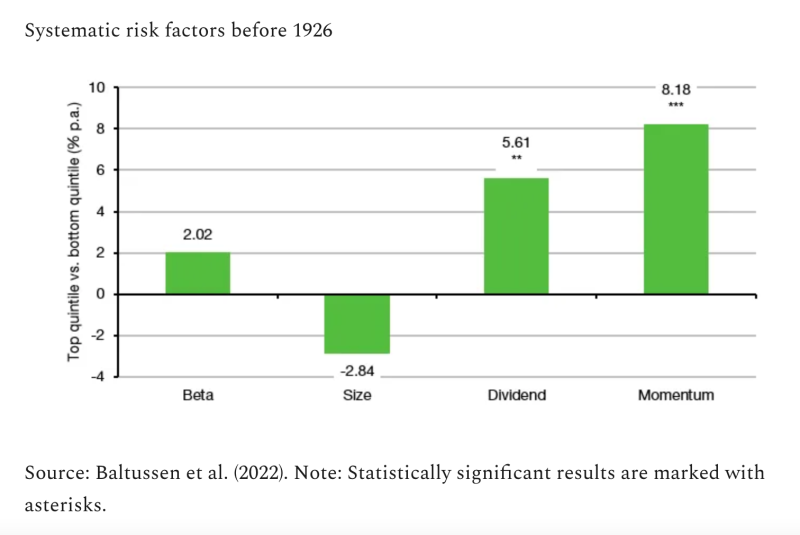

And this is where I have to congratulate the excellent research team at Robeco Quantitative Investments around Bart van Vliet to their work. They have created a comprehensive database of US stock returns, and dividends for the years 1866 to 1926. Based on this data they can test some of the most prominent risk factors for the sixty years before the CRSP data kicks in. they tested five systematic risk factors for both small cap and large cap stocks and the total US stock market. I want to focus here on the four most prominent factors: value (measured as dividend yield), momentum (measured as the 12M-1M price momentum), size (measured as market cap of the company), and Beta (measured as the CAPM beta).

The chart below shows the annual performance difference between the top 20% and bottom 20% of stocks by these four criteria. Results that are statistically significant are marked with asterisks.

I have to say, I love these results, because they confirm what Cam Harvey and his team have found. The CAPM does not hold in the data before 1926. Yes, there is a return difference between low beta and high beta stocks, but it is not significant and much smaller than the CAPM predicts. In fact, the slope of the capital market line is just 0.02, i.e. there is practically no correlation between the “systematic risk” of a stock as measured by the CAPM and its return.

Little evidence of a small-cap effect

Unfortunately, there is also little evidence that small-cap stocks outperform large-cap stocks. The return difference between small and large stocks is again not statistically significant and the correlation between market cap of a company and share price returns is essentially zero.

However, the two systematic risk factors that Cam Harvey and his team identified as above suspicion in his analysis of three hundred factors also show up as significant systematic risk factors before 1926: Both value and momentum provided statistically and economically significant outperformance. Note that I do not claim that this makes the case for value and momentum stronger. That would be a case of confirmation bias. No, all I say is that there is no falsification for these risk factors from this new data set so I can continue in my belief that value and momentum work.

But the fact that the CAPM fails before 1926 and that there is no small cap outperformance is interesting. It does not mean that these effects don’t exist. But it adds to the weight of evidence against these factors and we need to better understand why these factors fail to deliver returns before 1926.

In the case of the missing small-cap effect, I could well imagine that stock markets before 1926 were highly inefficient in incorporating information about companies into the share price. News travelled slowly and equity market investing was a niche corner of financial markets with low liquidity and a lot of market manipulation. The lack of liquidity affected all stocks, not just small caps. But where there is no liquidity, there is no efficient incorporation of news in prices. And that means that effectively all stocks, be it large or small, are mispriced all the time. This on the other hand can explain why small caps did not experience outperformance over large caps if the small-cap effect is due to a lack of efficient price discovery in small caps vs large caps. It’s one possibility, but we need more research to understand this result.

No comments:

Post a Comment

Note: Only a member of this blog may post a comment.