SOURCE:

Credit Bubble Bulletin : Weekly Commentary: Super Credit Bubble

My easy to read summary follows: Ye Editor

For the Week Ending September 2, 2022:

FINANCIAL DATA:

FINANCIAL DATA:

S&P500 dropped 3.3% (down 17.7% y-t-d)

Dow Industrials fell 3.0% (down 13.8%)

Utilities declined 1.6% (up 2.9%)

Banks lost 2.5% (down 20.6%)

Broker/Dealers slumped 2.7% (down 10.5%)

Transports sank 4.5% (down 16.6%)

S&P 400 Midcaps dropped 4.3% (down 15.8%)

Small cap Russell 2000 fell 4.7% (down 19.4%)

Nasdaq100 stumbled 4.0% (down 25.9%)

Semiconductors sank 7.1% (down 34.1%)

Biotechs slipped 0.6% (down 14.8%).

With gold bullion down $26,

the HUI gold equities index dropped 5.2%

(down 27.6%)

U.K.'s FTSE fell 2.0% (down 1.4% y-t-d).

Japan's Nikkei sank 3.5% (down 4.0% y-t-d).

Japan's Nikkei sank 3.5% (down 4.0% y-t-d).

France's CAC40 fell 1.7% (down 13.8%)

German DAX recovered 0.6% (down 17.8%).

Spain's IBEX 35 slumped 1.6% (down 9.0%).

Italy's FTSE MIB was about unchanged (down 19.8%).

Brazil's Bovespa declined 1.3% (up 5.8%)

Mexico's Bolsa dropped 2.9% (down 13.9%).

South Korea's Kospi dropped 2.9% (down 19.1%).

India's Sensex was little changed (up 0.9%).

China's Shanghai lost 1.5% (down 12.5%).

Turkey's Istanbul National 100 gained 2.4% (up 73.5%).

Russia's MICEX rallied 8.9% (down 34.7%).

Three-month Treasury bill rates ended the week at 2.8075%.

Two-year government yields slipped a basis point to 3.39%

(up 266bps y-t-d).

Five-year T-note yields rose nine bps to 3.29%

(up 203bps).

Ten-year Treasury yields jumped 15 bps to 3.19%

(up 168bps).

Long bond yields rose 15 bps to 3.35%

up 144bps).

Benchmark Fannie Mae MBS yields surged 19 bps to 4.68%

up 261bps).

Federal Reserve Credit last week declined $21.6bn to $8.797 TN. Fed Credit is down $92.7bn from the June 22nd peak.

Over the past 155 weeks, Fed Credit expanded $5.070 TN, or 136%.

Freddie Mac 30-year fixed mortgage rates rose 11 bps to a nine-week high 5.66% (up 279bps y-o-y).

Freddie Mac 30-year fixed mortgage rates rose 11 bps to a nine-week high 5.66% (up 279bps y-o-y).

Fifteen-year rates gained 13 bps to 4.98% (up 280bps).

Five-year hybrid ARM rates jumped 15 bps to 4.51% (up 208bps).

Jumbo mortgage 30-year fixed rates up 23 bps to 6.10% (up 306bps).

For the week, the U.S. Dollar Index increased 0.7% to 109.53 (up 14.5% y-t-d). The Chinese (onshore) renminbi declined 0.41% versus the dollar (down 7.88% y-t-d).

The Bloomberg Commodities Index sank 4.4% (up 20.1% y-t-d).

Spot Gold declined 1.5% to $1,712 (down 6.4%).

Silver dropped 4.5% to $18.04 (down 22.6%).

WTI crude sank $6.19 to $86.87 (up 16%).

Gasoline fell 13.6% (up 11%)

Natural Gas dropped 5.5% to $8.79 (up 136%).

Copper sank 7.7% (down 24%).

Wheat increased 0.7% (up 5%)

Corn added 0.2% (up 12%).

Bitcoin slumped $700, or 3.4%,

this week to $19,960 (down 57%).

ECONOMIC NEWS:

September 1 – Financial Times (Max Seddon, Nastassia Astrasheuskaya and Roman Olearchyk): “Vladimir Putin has called Ukraine ‘an anti-Russian enclave’ as Moscow delivered a renewed threat to western efforts to curb surging energy prices. Speaking in the Russian exclave of Kaliningrad…, Putin said of Ukraine: ‘Our guys who are fighting there are defending both the residents of Donbas [the industrial area in the east largely occupied by Russia] and defending Russia itself,’ according to news agency Interfax. ‘They started creating an anti-Russian enclave on the territory of today’s Ukraine that is threatening our country,’ Putin said.”

September 2 – Bloomberg: “Russia’s Gazprom… said its key gas pipeline to Europe won’t reopen as planned, moving the region a step closer to blackouts, rationing and a severe recession. The pipeline was due to reopen on Saturday after maintenance. But in a last-minute move late Friday, the company said a technical issue had been found and the pipe can’t operate again until it’s fixed. The European Union said Gazprom was acting on ‘fallacious pretenses,’ and Siemens Energy, which makes the pipeline’s turbines, said what Gazprom had found didn’t justify cutting the gas. It’s a massive blow to Europe, which is scrambling to cut its dependency on Russian gas before winter and has been waiting for Moscow’s next steps in the energy war.”

August 31 – Reuters (Christoph Steitz and Nina Chestney): “Russia halted gas supplies via Europe's key supply route on Wednesday, intensifying an economic battle between Moscow and Brussels and raising the prospects of recession and energy rationing in some of the region's richest countries. European governments fear Moscow could extend the outage in retaliation for Western sanctions imposed after it invaded Ukraine and have accused Russia of using energy supplies as a ‘weapon of war’. Moscow denies doing this and has cited technical reasons for supply cuts.”

September 2 – Reuters: “The Kremlin said… that Russia would stop selling oil to countries that impose price caps on Russia's energy resources - caps that Moscow said would lead to significant destabilisation of the global oil market. ‘Companies that impose a price cap will not be among the recipients of Russian oil,’ Kremlin spokesman Dmitry Peskov told reporters…”

August 30 – Financial Times (Sarah White and David Sheppard): “Gazprom is set to halt all gas deliveries to French utility Engie from Thursday, citing a payment dispute, adding to concerns over Russian supplies to Europe over the coming weeks as France and its neighbours search for alternatives. The Russian state-owned gas group said… it would suspend Engie’s deliveries in full from September 1 until the row had been resolved… Engie, which is France’s biggest supplier of gas to households and companies, had earlier warned its Russian deliveries would be reduced, citing a disagreement ‘on the application of some contracts’.”

August 29 – Reuters (Supantha Mukherjee and Alexander Marrow): “Western technology companies, including Ericsson and Nokia, announced plans for complete exits from Russia on Monday, following Dell last week, as the pace of withdrawals accelerates. Ericsson said it will gradually withdraw from Russia over the coming months, while its Finnish rival Nokia said it also plans to exit its Russian business by the end of the year. Switzerland-based Logitech International also said it would wind down its remaining activities in Russia… More western companies are selling or withdrawing from their Russian businesses, having initially halted operations after Moscow sent tens of thousands of troops into Ukraine on Feb. 24.”

August 31 – Reuters (Stephen Nellis and Jane Lanhee Lee): “Chip designer Nvidia Corp said… that U.S. officials told it to stop exporting two top computing chips for artificial intelligence work to China, a move that could cripple Chinese firms' ability to carry out advanced work like image recognition and hamper Nvidia's business in the country. The announcement signals a major escalation of the U.S. crackdown on China's technological capabilities as tensions bubble over the fate of Taiwan, where chips for Nvidia and almost every other major chip firm are manufactured.”

September 1 – Bloomberg (Elizabeth Elkin): “The cost to grow food is soaring according to a new US report, a sign that inflation and its worst effects, such as hunger, aren’t over. Everything that farmers use to cultivate crops from fertilizer to feed and labor are skyrocketing in price. Production costs are estimated to rise by $66.2 billion or 18% in 2022, the most ever, according to the US Department of Agriculture.”

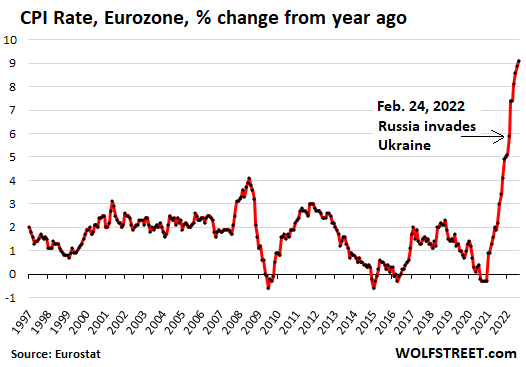

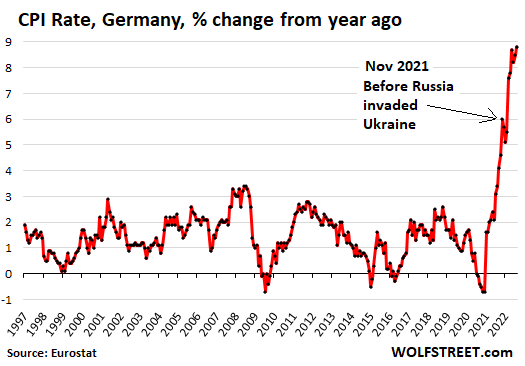

August 30 – Financial Times (Martin Arnold): “German inflation accelerated to a 40-year high of 8.8% in the year to August, bolstering calls for the European Central Bank to accelerate the pace of interest rate rises when its policymakers meet next week. Consumer prices in Europe’s largest economy were mostly driven by the soaring cost of energy and food, lifting inflation 0.4 percentage points from July despite recent government measures to cushion the blow for households. The figures supported calls by ECB governing council members for the bank to be more aggressive in its policy response to the surge in inflation, which has hit its highest level since the euro was created 23 years ago and is expected to have accelerated further in August.”

September 2 – CNBC (Jeff Cox): “Nonfarm payrolls rose solidly in August amid an otherwise slowing economy, while the unemployment rate ticked higher as more workers rejoined the labor force… The economy added 315,000 jobs for the month, just below the… estimate for 318,000 and well off the 526,000 in July… The unemployment rate rose to 3.7%, two-tenths of a percentage point higher than expectations largely due to a rising labor force participation rate… Wages continued to rise, though slightly less than expectations. Average hourly earnings increased 0.3% for the month and 5.2% from a year ago, both 0.1 percentage point below estimates. Professional and business services led payroll gains with 68,000, followed by health care with 48,000 and retail with 44,000. Leisure and hospitality… rose by just 31,000 for the month after averaging 90,000 in the previous seven months of 2022.”

September 1 – CNBC (Jeff Cox): “Initial filings for unemployment insurance fell to their lowest level since late June last week, a sign that the labor market is resilient amid a slowing economy. Claims totaled a seasonally adjusted 232,000 for the week ended Aug. 27, a decline of 5,000 from the previous period and the lowest since June 25… Economists… had been looking for 245,000. Continuing claims increased to 1.44 million, up 26,000 from the previous level in data that runs a week behind the headline number.”

August 31 – CNBC (Jeff Cox): “Companies sharply slowed the pace of hiring in August amid growing fears of an economic slowdown, according to payroll processing company ADP. Private payrolls grew by just 132,000 for the month, a deceleration from the 268,000 gain in July… ‘Our data suggests a shift toward a more conservative pace of hiring, possibly as companies try to decipher the economy’s conflicting signals,’ said ADP’s chief economist, Nela Richardson. ‘We could be at an inflection point, from super-charged job gains to something more normal.’ August payroll numbers are notoriously volatile.”

August 31 – CNBC (Diana Olick): “After falling back earlier this month, mortgage rates began rising sharply again to the highest level since mid-July. That caused mortgage demand to pull back even further. Total mortgage application volume fell 3.7% last week compared with the previous week… Volume was 63% lower than the same week one year ago… Mortgage applications to purchase a home dropped 2% for the week and were 23% lower than the same week one year ago. ‘Purchase applications have declined in eight of the last nine weeks, as demand continues to shrink due to higher rates and a weaker economic outlook,’ Kan said.”

August 29 – Bloomberg (Martine Paris): “For cash-strapped renters, the situation is getting more dire in many US metro areas. The Zumper National Rent Index shows the median national one-bedroom rent for a newly listed one-bedroom now at $1,486, up 11.8% over August 2021 — beating last month’s record high. More than half of US cities are showing double-digit rent hikes, with some over 30%. New York City continues to be the priciest place to be a tenant, with median one-bedroom rent up 39.9% year-over-year; those with two-bedroom apartments are paying 46.7% more. Manhattan leads the boroughs, with monthly rent climbing to $4,212, up 27% over last year.”

August 30 – Bloomberg: “China’s factory activity contracted in August for a second straight month, with the economy taking a hit from power shortages spurred by a historic drought, on top of a property market crisis and Covid outbreaks. The official manufacturing purchasing managers index rose to 49.4 from 49 in July… The non-manufacturing gauge, which measures activity in the construction and services sectors, fell to 52.6 from 53.8 in July… What Bloomberg’s Economists Say... ‘China’s August PMIs confirmed signals from high-frequency data -- the economy continued to lose speed over the summer. Multiple shocks took a toll, ranging from Covid-19 outbreaks to power shortages, on top of pressures from the property slump.’”

August 31 – Bloomberg: “The Chinese metropolis of Chengdu locked down its 21 million residents to contain a Covid-19 outbreak, a seismic move in the country’s vast Western region that has largely been untouched by the virus. The capital of Sichuan province, Chengdu is the biggest city to shut down since Shanghai’s bruising two-month lockdown earlier this year. The move… shows the country’s commitment to the Covid Zero approach espoused by President Xi Jinping, despite the disruption it’s causing.”

August 30 – Wall Street Journal (Rebecca Feng): “One of China’s largest developers said the country’s property market has tumbled into a severe depression, using some of the strongest language yet to describe the yearlong downturn and the financial pain it has caused. Country Garden… reported a 96% drop in first-half profit after selling a third fewer homes than it did a year ago. The… company said the market has struggled with weakening expectations, sluggish demand and declines in property prices. ‘All these exert mounting pressure on all participants in the property market, which has slid rapidly into severe depression,’ the company said. It added that the resurgence of Covid-19 in cities across China has also slowed construction activity and weighed on its performance.”

September 1 – Reuters (Jonathan Cable and Leika Kihara): “Global factory activity slumped in August as Russia's war in Ukraine and China's zero COVID-19 curbs continued to hurt businesses…, although there were indications cost pressures were starting to ease. Manufacturing activity was weak in countries ranging from Germany to Britain to China in a sign sluggish demand was adding to headaches for companies already suffering from lingering supply constraints… S&P Global's final euro zone manufacturing Purchasing Managers' Index (PMI) dipped to 49.6 in August from July's 49.8, edging further below the 50 mark separating growth from contraction.”

September 2 – Bloomberg (Ari Altstedter): “Toronto home prices fell for a fifth straight month, the longest skid since 2017… The benchmark price for a home in Canada’s largest city dropped 2.8% in August compared with the month before to reach C$1.12 million (about $854,000), according to… the Toronto Regional Real Estate Board. That brings the total price decline to nearly 16% since March -- the biggest five-month drop since the measure started being tracked in 2005.”

August 31 – Bloomberg (Mark Chediak and David R. Baker): “California officials declared a statewide grid emergency to cope with surging demand for power amid a blistering heat wave, raising the prospect of rolling blackouts. The California Independent System Operator issued a level-1 energy emergency alert around 3:10 p.m. local time Wednesday after tapping all of its available power supplies. The notice, which comes after officials asked homes and businesses to conserve, is a warning that the state is anticipating power shortages. It’s the biggest test for California’s grid since the summer of 2020, when rolling outages engulfed portions of the state.”

ECONOMIC NEWS:

September 2 – Bloomberg (Garfield Reynolds and Finbarr Flynn): “Under pressure from central bankers determined to quash inflation even at the cost of a recession, global bonds slumped into their first bear market in a generation. The Bloomberg Global Aggregate Total Return Index of government and investment-grade corporate bonds has fallen more than 20% from its 2021 peak on an unhedged basis, the biggest drawdown since its inception in 1990.”

September 2 – Bloomberg: “Russia’s Gazprom… said its key gas pipeline to Europe won’t reopen as planned, moving the region a step closer to blackouts, rationing and a severe recession. The pipeline was due to reopen on Saturday after maintenance. But in a last-minute move late Friday, the company said a technical issue had been found and the pipe can’t operate again until it’s fixed. The European Union said Gazprom was acting on ‘fallacious pretenses,’ and Siemens Energy, which makes the pipeline’s turbines, said what Gazprom had found didn’t justify cutting the gas. It’s a massive blow to Europe, which is scrambling to cut its dependency on Russian gas before winter and has been waiting for Moscow’s next steps in the energy war.”

August 31 – Reuters (Christoph Steitz and Nina Chestney): “Russia halted gas supplies via Europe's key supply route on Wednesday, intensifying an economic battle between Moscow and Brussels and raising the prospects of recession and energy rationing in some of the region's richest countries. European governments fear Moscow could extend the outage in retaliation for Western sanctions imposed after it invaded Ukraine and have accused Russia of using energy supplies as a ‘weapon of war’. Moscow denies doing this and has cited technical reasons for supply cuts.”

September 2 – Reuters: “The Kremlin said… that Russia would stop selling oil to countries that impose price caps on Russia's energy resources - caps that Moscow said would lead to significant destabilisation of the global oil market. ‘Companies that impose a price cap will not be among the recipients of Russian oil,’ Kremlin spokesman Dmitry Peskov told reporters…”

August 30 – Financial Times (Sarah White and David Sheppard): “Gazprom is set to halt all gas deliveries to French utility Engie from Thursday, citing a payment dispute, adding to concerns over Russian supplies to Europe over the coming weeks as France and its neighbours search for alternatives. The Russian state-owned gas group said… it would suspend Engie’s deliveries in full from September 1 until the row had been resolved… Engie, which is France’s biggest supplier of gas to households and companies, had earlier warned its Russian deliveries would be reduced, citing a disagreement ‘on the application of some contracts’.”

August 29 – Reuters (Supantha Mukherjee and Alexander Marrow): “Western technology companies, including Ericsson and Nokia, announced plans for complete exits from Russia on Monday, following Dell last week, as the pace of withdrawals accelerates. Ericsson said it will gradually withdraw from Russia over the coming months, while its Finnish rival Nokia said it also plans to exit its Russian business by the end of the year. Switzerland-based Logitech International also said it would wind down its remaining activities in Russia… More western companies are selling or withdrawing from their Russian businesses, having initially halted operations after Moscow sent tens of thousands of troops into Ukraine on Feb. 24.”

August 31 – Reuters (Stephen Nellis and Jane Lanhee Lee): “Chip designer Nvidia Corp said… that U.S. officials told it to stop exporting two top computing chips for artificial intelligence work to China, a move that could cripple Chinese firms' ability to carry out advanced work like image recognition and hamper Nvidia's business in the country. The announcement signals a major escalation of the U.S. crackdown on China's technological capabilities as tensions bubble over the fate of Taiwan, where chips for Nvidia and almost every other major chip firm are manufactured.”

September 1 – Bloomberg (Elizabeth Elkin): “The cost to grow food is soaring according to a new US report, a sign that inflation and its worst effects, such as hunger, aren’t over. Everything that farmers use to cultivate crops from fertilizer to feed and labor are skyrocketing in price. Production costs are estimated to rise by $66.2 billion or 18% in 2022, the most ever, according to the US Department of Agriculture.”

August 30 – Financial Times (Martin Arnold): “German inflation accelerated to a 40-year high of 8.8% in the year to August, bolstering calls for the European Central Bank to accelerate the pace of interest rate rises when its policymakers meet next week. Consumer prices in Europe’s largest economy were mostly driven by the soaring cost of energy and food, lifting inflation 0.4 percentage points from July despite recent government measures to cushion the blow for households. The figures supported calls by ECB governing council members for the bank to be more aggressive in its policy response to the surge in inflation, which has hit its highest level since the euro was created 23 years ago and is expected to have accelerated further in August.”

September 2 – CNBC (Jeff Cox): “Nonfarm payrolls rose solidly in August amid an otherwise slowing economy, while the unemployment rate ticked higher as more workers rejoined the labor force… The economy added 315,000 jobs for the month, just below the… estimate for 318,000 and well off the 526,000 in July… The unemployment rate rose to 3.7%, two-tenths of a percentage point higher than expectations largely due to a rising labor force participation rate… Wages continued to rise, though slightly less than expectations. Average hourly earnings increased 0.3% for the month and 5.2% from a year ago, both 0.1 percentage point below estimates. Professional and business services led payroll gains with 68,000, followed by health care with 48,000 and retail with 44,000. Leisure and hospitality… rose by just 31,000 for the month after averaging 90,000 in the previous seven months of 2022.”

September 1 – CNBC (Jeff Cox): “Initial filings for unemployment insurance fell to their lowest level since late June last week, a sign that the labor market is resilient amid a slowing economy. Claims totaled a seasonally adjusted 232,000 for the week ended Aug. 27, a decline of 5,000 from the previous period and the lowest since June 25… Economists… had been looking for 245,000. Continuing claims increased to 1.44 million, up 26,000 from the previous level in data that runs a week behind the headline number.”

August 31 – CNBC (Jeff Cox): “Companies sharply slowed the pace of hiring in August amid growing fears of an economic slowdown, according to payroll processing company ADP. Private payrolls grew by just 132,000 for the month, a deceleration from the 268,000 gain in July… ‘Our data suggests a shift toward a more conservative pace of hiring, possibly as companies try to decipher the economy’s conflicting signals,’ said ADP’s chief economist, Nela Richardson. ‘We could be at an inflection point, from super-charged job gains to something more normal.’ August payroll numbers are notoriously volatile.”

August 31 – CNBC (Diana Olick): “After falling back earlier this month, mortgage rates began rising sharply again to the highest level since mid-July. That caused mortgage demand to pull back even further. Total mortgage application volume fell 3.7% last week compared with the previous week… Volume was 63% lower than the same week one year ago… Mortgage applications to purchase a home dropped 2% for the week and were 23% lower than the same week one year ago. ‘Purchase applications have declined in eight of the last nine weeks, as demand continues to shrink due to higher rates and a weaker economic outlook,’ Kan said.”

August 29 – Bloomberg (Martine Paris): “For cash-strapped renters, the situation is getting more dire in many US metro areas. The Zumper National Rent Index shows the median national one-bedroom rent for a newly listed one-bedroom now at $1,486, up 11.8% over August 2021 — beating last month’s record high. More than half of US cities are showing double-digit rent hikes, with some over 30%. New York City continues to be the priciest place to be a tenant, with median one-bedroom rent up 39.9% year-over-year; those with two-bedroom apartments are paying 46.7% more. Manhattan leads the boroughs, with monthly rent climbing to $4,212, up 27% over last year.”

August 30 – Bloomberg: “China’s factory activity contracted in August for a second straight month, with the economy taking a hit from power shortages spurred by a historic drought, on top of a property market crisis and Covid outbreaks. The official manufacturing purchasing managers index rose to 49.4 from 49 in July… The non-manufacturing gauge, which measures activity in the construction and services sectors, fell to 52.6 from 53.8 in July… What Bloomberg’s Economists Say... ‘China’s August PMIs confirmed signals from high-frequency data -- the economy continued to lose speed over the summer. Multiple shocks took a toll, ranging from Covid-19 outbreaks to power shortages, on top of pressures from the property slump.’”

August 31 – Bloomberg: “The Chinese metropolis of Chengdu locked down its 21 million residents to contain a Covid-19 outbreak, a seismic move in the country’s vast Western region that has largely been untouched by the virus. The capital of Sichuan province, Chengdu is the biggest city to shut down since Shanghai’s bruising two-month lockdown earlier this year. The move… shows the country’s commitment to the Covid Zero approach espoused by President Xi Jinping, despite the disruption it’s causing.”

August 30 – Wall Street Journal (Rebecca Feng): “One of China’s largest developers said the country’s property market has tumbled into a severe depression, using some of the strongest language yet to describe the yearlong downturn and the financial pain it has caused. Country Garden… reported a 96% drop in first-half profit after selling a third fewer homes than it did a year ago. The… company said the market has struggled with weakening expectations, sluggish demand and declines in property prices. ‘All these exert mounting pressure on all participants in the property market, which has slid rapidly into severe depression,’ the company said. It added that the resurgence of Covid-19 in cities across China has also slowed construction activity and weighed on its performance.”

September 1 – Reuters (Jonathan Cable and Leika Kihara): “Global factory activity slumped in August as Russia's war in Ukraine and China's zero COVID-19 curbs continued to hurt businesses…, although there were indications cost pressures were starting to ease. Manufacturing activity was weak in countries ranging from Germany to Britain to China in a sign sluggish demand was adding to headaches for companies already suffering from lingering supply constraints… S&P Global's final euro zone manufacturing Purchasing Managers' Index (PMI) dipped to 49.6 in August from July's 49.8, edging further below the 50 mark separating growth from contraction.”

September 2 – Bloomberg (Ari Altstedter): “Toronto home prices fell for a fifth straight month, the longest skid since 2017… The benchmark price for a home in Canada’s largest city dropped 2.8% in August compared with the month before to reach C$1.12 million (about $854,000), according to… the Toronto Regional Real Estate Board. That brings the total price decline to nearly 16% since March -- the biggest five-month drop since the measure started being tracked in 2005.”

August 31 – Bloomberg (Mark Chediak and David R. Baker): “California officials declared a statewide grid emergency to cope with surging demand for power amid a blistering heat wave, raising the prospect of rolling blackouts. The California Independent System Operator issued a level-1 energy emergency alert around 3:10 p.m. local time Wednesday after tapping all of its available power supplies. The notice, which comes after officials asked homes and businesses to conserve, is a warning that the state is anticipating power shortages. It’s the biggest test for California’s grid since the summer of 2020, when rolling outages engulfed portions of the state.”

August 28 – Bloomberg (Kim Chipman and Tarso Veloso): “Drought is shrinking crops from the US Farm Belt to China’s Yangtze River basin, ratcheting up fears of global hunger and weighing on the outlook for inflation. The latest warning flare comes out of the American Midwest, where some corn is so parched stalks are missing ears of grain and soybean pods are fewer and smaller than usual. The dismal report from the Pro Farmer Crop Tour has helped lift a gauge of grain prices back to the highest level since June. The world is desperate to replenish grain reserves diminished by trade disruptions in the Black Sea and unfavorable weather in some of the largest growing regions.”

DOUG NOLAND'S COMMENTARY:

highly edited

full version at the link below:

Global “Risk Off” gathers momentum by the week. Crisis ... as global central banks coalesce around a united front for battling inflation. The reality that central bankers will aggressively hike rates until something breaks has begun to sink in. Last Friday’s Jackson Hole selling pressure carried over into this week for U.S. equities.

August 31 – Bloomberg (Alexander Weber): “Euro-area inflation accelerated to another all-time high, strengthening the case for the European Central Bank to consider a jumbo interest-rate hike when it meets next week. Consumer prices in the 19-nation currency bloc jumped 9.1% from a year ago in August… The question now is whether the data are enough to nudge the ECB toward the 75 bps rate increase that some on its 25-strong Governing Council want debated… ‘There’s an urgent need for the Governing Council to act decisively at its next meeting to combat inflation,’ ...

And with the Bank of England fixated on its inflation fight, UK yields surged 32 bps this week to 2.91% - the high since January 2014. UK yields have surged 105 bps over the past month.

Meanwhile, the yen (vs. $) dropped further to a 24-year low, ...

Commodities are in the grips of global “Risk Off” dynamics. The Bloomberg Commodities Index dropped 4.4% this week. Crude sank 6.7% ($6.19), Gasoline 13.6%, Copper 7.7%, Nickel 5.3%, Tin 13.0%, Zinc 11.6%, Iron Ore 9.4%, Aluminum 5.7%, Coffee 3.9%, Cotton 11.2%, and Soybeans 5.9%. I assume the global leveraged speculating community is running for cover.

Commodities are in the grips of global “Risk Off” dynamics. The Bloomberg Commodities Index dropped 4.4% this week. Crude sank 6.7% ($6.19), Gasoline 13.6%, Copper 7.7%, Nickel 5.3%, Tin 13.0%, Zinc 11.6%, Iron Ore 9.4%, Aluminum 5.7%, Coffee 3.9%, Cotton 11.2%, and Soybeans 5.9%. I assume the global leveraged speculating community is running for cover.

September 2 - New York Post (Thomas Barrabi): “Despite a summer rally, the US stock market is still an unprecedented ‘superbubble’ that will cause financial ‘tragedy’ for investors when it bursts, famed investor Jeremy Grantham predicted. The co-founder of the asset-management firm GMO… said the current superbubble was entering its ‘final act’ due to deteriorating economic conditions. A recent ‘bear-market rally’ that saw the S&P 500 recoup 58% of its losses from a June low follows the pattern of past stock-market crashes in 1929, 1973 and 2000...

‘The current superbubble features an unprecedentedly dangerous mix of cross-asset overvaluation (with bonds, housing and stocks all critically overpriced and now rapidly losing momentum), commodity shock and Fed hawkishness,’ Grantham wrote... ‘Each cycle is different and unique - but every historical parallel suggests that the worst is yet to come.’”

Jeremy Grantham has enjoyed a long and distinguished career. He accurately predicted bursting stock market Bubbles in Japan in the late-eighties, along with the U.S. equities Bubbles in the late-nineties and again in 2008. Grantham will surely only solidify Wall Street legend status with his latest “superbubble” call.

... The U.S. stock market “superbubble” is a manifestation of history’s greatest global Credit Bubble. Moreover, the post-2008 crisis “blow-off” finale saw unprecedented debt growth span the globe, with epic inflation at the very core of global finance – perceived safe central bank Credit and government debt.

Grantham: “Why are the historic superbubbles always followed by major economic setbacks? Perhaps because they occurred after a very extended build-up of market and economic forces – with a major surge of optimism thrown in at the end.”

... Why was the post-mortgage finance Bubble economic downturn much deeper than the post-tech Bubble recession? Because Credit system impairment was significantly more severe.

Jeremy Grantham has enjoyed a long and distinguished career. He accurately predicted bursting stock market Bubbles in Japan in the late-eighties, along with the U.S. equities Bubbles in the late-nineties and again in 2008. Grantham will surely only solidify Wall Street legend status with his latest “superbubble” call.

... The U.S. stock market “superbubble” is a manifestation of history’s greatest global Credit Bubble. Moreover, the post-2008 crisis “blow-off” finale saw unprecedented debt growth span the globe, with epic inflation at the very core of global finance – perceived safe central bank Credit and government debt.

Grantham: “Why are the historic superbubbles always followed by major economic setbacks? Perhaps because they occurred after a very extended build-up of market and economic forces – with a major surge of optimism thrown in at the end.”

... Why was the post-mortgage finance Bubble economic downturn much deeper than the post-tech Bubble recession? Because Credit system impairment was significantly more severe.

Importantly, a crisis of confidence in risky mortgage Credit poisoned the liabilities of highly levered financial institutions, fostering disruption and a dramatic slowdown in Credit growth (an actual contraction of mortgage Credit).

The Great Depression was more the fallout from a crisis of confidence in debt and banking systems than a direct consequence of the 1929 stock market crash.

The Great Depression was more the fallout from a crisis of confidence in debt and banking systems than a direct consequence of the 1929 stock market crash.

Super Credit Bubbles inevitably end in crisis.

The heart of the matter: an untenable mountain of debt is supported by a deeply maladjusted economic structure.

I could not agree more with Jeremy Grantham.

I’ll refer to data from the IIF’s May Global Debt Monitor: “Total global debt rose by $3.3 trillion in Q1 2022 to a new record of over $305 trillion – mostly due to the U.S. and China.”

Comparing Q1 2022 to pre-Covid Q3 2019 (10 quarters), total global debt surged $52.9 TN, or 20.9%.

Over this period, emerging market (EM) debt expanded $26.2 TN, or 36.1%, led by a 47% surge in EM government debt and a 32.6% increase in EM non-financial corporate debt.